Before we get into Trigger rate, let’s talk about Variable Rates.

There are two types of Variable Rates. One with a static payment (VRM) where payments stay the same even if interest increases and one with an adjustable payment (ARM) that fluctuate with prime rate.

If you have a variable rate and your payments have not changed, you definitely have a VRM.

In a VRM, some portion of your payment goes towards interest and some towards principal. This means, when prime rate increases, your static payments don’t change, just more of your payment goes towards interest and less towards principal.

We’ve talked about the difference between VRM and ARM in greater detail in our blog here.

The Trigger Point

There is a point (a trigger point) where prime rate has increased so much that your entire mortgage payment can only cover the interest accrued. At this point, your static payment is forced to increase just to cover any additional interest.

For the other type of Variable rate (ARM), where the payments adjust automatically (ARM), the trigger rate/point concept has no meaning because every time the prime changes, the payments are updated to cover interest and principal.

What happens at the trigger point?

Lenders may ask clients to choose from three options: (1) Increase regular payments to cover the interest, (2) Make lump-sum pre-payments OR (3) lock in with a fixed interest rate.

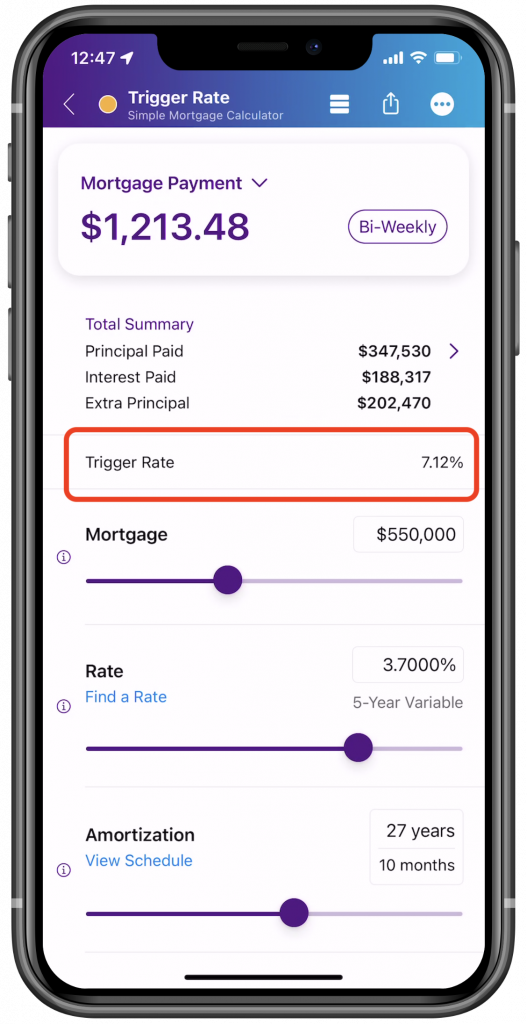

How to Calculate the Trigger Rate

Use the Simple Mortgage Calculator

You can use the “Simple Mortgage Calculator” feature to calculate the trigger rate.

Just need to enter the current mortgage balance, the current interest rate and the remaining amortization left on the mortgage. This will match the client’s current payments.

Please note: If you don’t see the trigger rate in the “Simple mortgage Calculator”, make sure that the rate type shows Variable under the current rate input. Tap on it to change it.

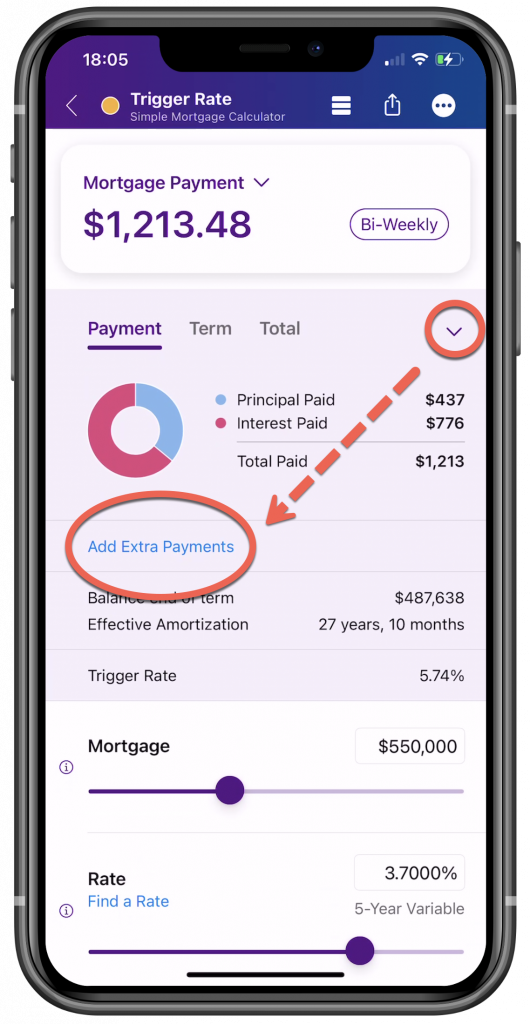

What if you were to increase your payment?

You guessed correctly. If you were to increase payment, there is now an additional buffer, and the trigger rate will have increased.

In fact, throughout the term, as principal decreases, the trigger rate increases.

Now you can actually simulate this and calculate a new trigger rate after applying extra payments using the same “Simple Mortgage Calculator”.

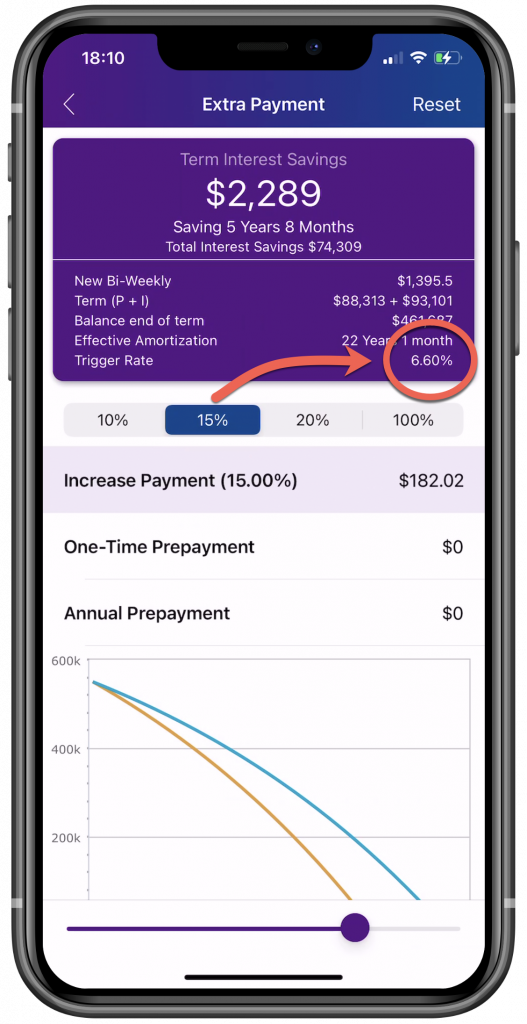

Bumping up the Trigger Rate

It’s as easy as increasing your payments to bump up the Trigger Rate.

In our example, we increased our payment by 15% and our trigger rate has bumped from 5.74% to 6.60%. That’s a 0.86% difference. This is HUGE!

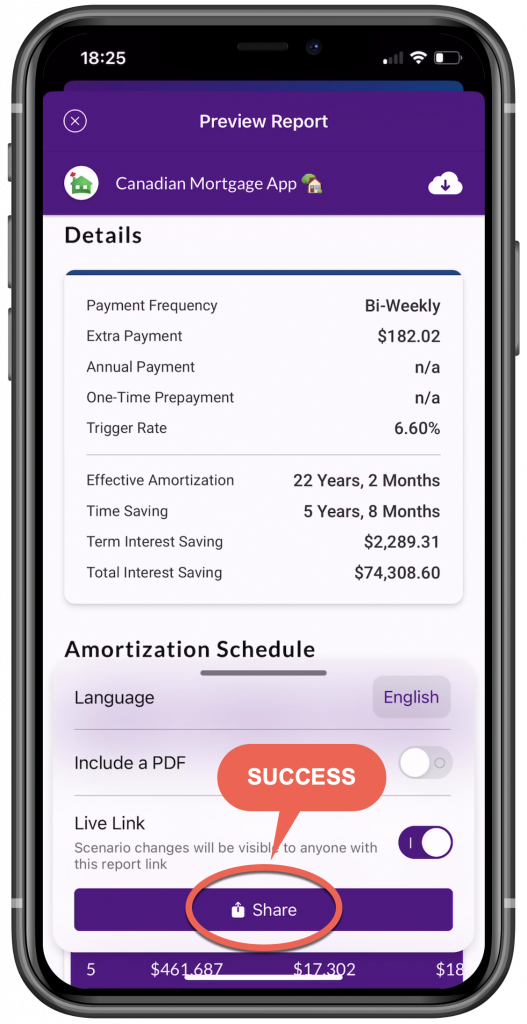

What are you waiting for?

Generate a report and let your client know that you got their backs and always looking for their best interest.

By sending a simple report to your clients, it demonstrates that you are always thinking about them and constantly running scenarios to ensure their financial well-being is looked after.

Quick Video

We put together a short video on how to use the app to calculate your trigger rates. Check it out here

I'm a réaltor in downtown Toronto and I make my clients download this app. It allows us to compare costs of various properties easily and accurately.

Keep up the good work!

As a real estate Broker this App is amazing for my clients. It helps them play around with different purchase price scenarios, calculate closing costs & down payments etc....it also helps me run quick numbers for investor clients on the spot. The Pro is worth it all day long! The support staff is great and very responsive.

I have been a mortgage broker for 12 years and this is the best mortgage calculator app that I have ever used.

I am very excited to share it with both my clients and referral sources!

Thank you!!

As a new real estate investor, this app is my number one go-to resource for quickly comparing and evaluating the properties I'm looking at. Great interface, and easy to use.

I'm a Real Estate Sales Professional in Ontario- this app covers it all! Land transfer tax calculations, mortgage insurance calculations, etc. They thought of everything when they developed this app!