You may have heard of the term “mortgage refinance” or “refi,” but do you truly understand what this means? In this article, we’re going to look at what a mortgage refinance is, as well as the reasons to refinance and the costs/fees of refinancing your mortgage.

What is a Mortgage Refinance?

A mortgage refinances when you renegotiate your current mortgage. This usually means breaking your current mortgage and starting a new one with your existing lender or a new lender. In order to refinance, you must have at least 20 percent equity in your home; otherwise, you can’t do it.

There are several reasons you might refinance your mortgage, which we’re going to discuss next.

Consolidating Debt

Do you have a lot of consumer debt as a result of COVID-19? You’re not alone. If your employment situation or business was affected by COVID-19, you might have had to borrow a lot of money to be able to pay the bills when times were tough. Even if times are better, it could take you a long time to pay off your newfound debt if you’re paying it off on your credit card at a rate of 18 percent or higher.

Consolidating your debt is a clean slate of sorts. When you refinance your mortgage and consolidate your debts, you take out a new mortgage that pays off your high-interest debts. Why would you do that? Because mortgage rates are pretty much the lowest interest rates of any debt out there. By locking in your consumer debt at such a low rate, you can pay your debts off sooner just by paying the same you were before due to the lowest interest rates. It’s a win-win.

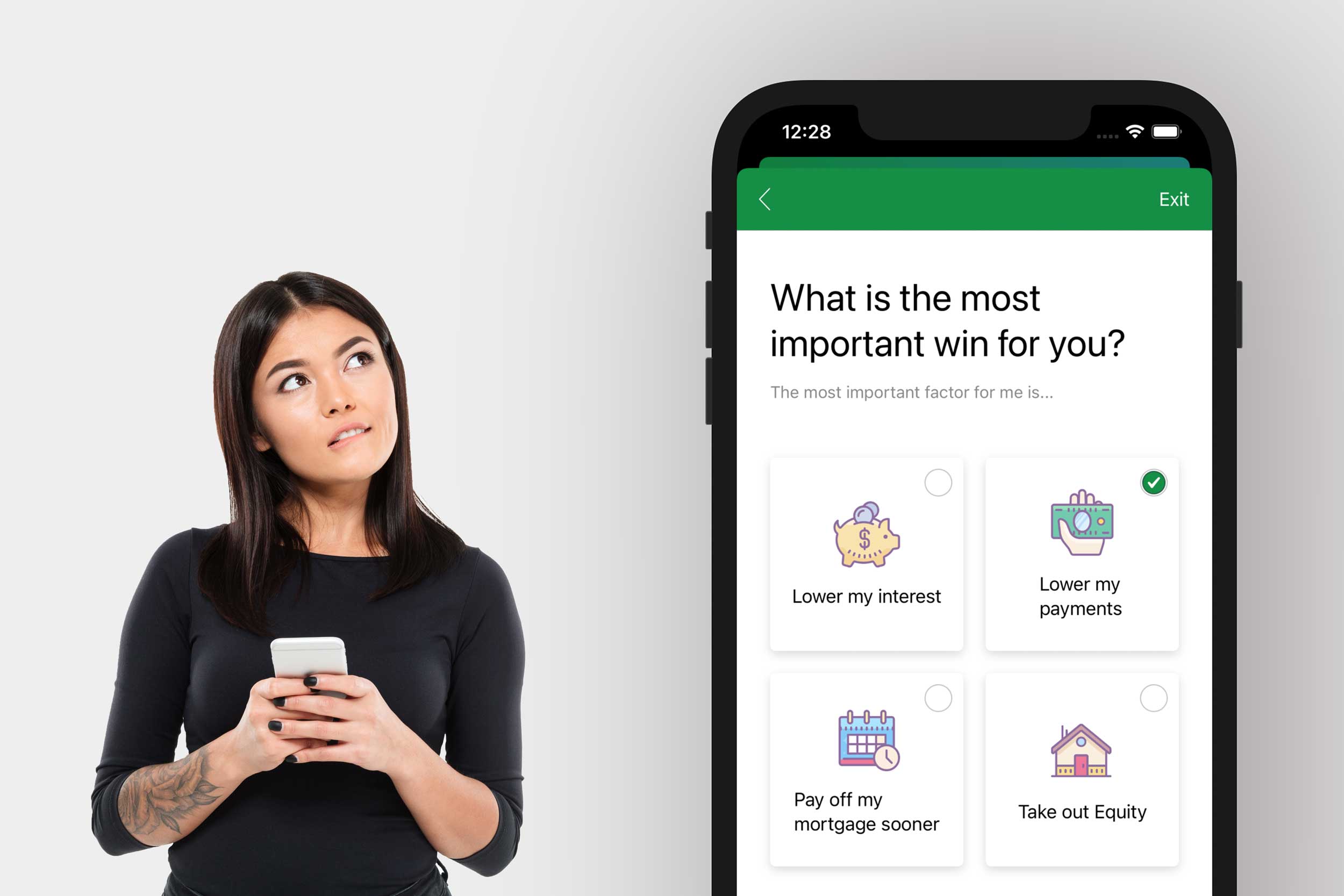

Lowering Your Monthly Payment

Are you finding your monthly mortgage payments too much of a drain on your cash flow? When you refinance your mortgage, you can stretch your amortization period (the total length of time it takes to pay off your mortgage) to 25 or 30 years; when you do that, your monthly mortgage payments become lower and more affordable.

Sure, it will cost you more interest over time, but it will provide you with the immediate cash flow relief you need. If your new lender has generous prepayment privileges, you can make extra payments to catch up when your cash flow situation improves.

Pull Out Equity for Home Renos

Are you thinking about adding a new kitchen or bathroom? Coming up with a spare $50k in savings can be tough. It could take you years to save. Why not use some of that home equity that’s just sitting there to pay for it?

You can borrow the funds as a Home Equity Line of Credit (HELOC) or a brand new mortgage. If you’re looking for the most flexibility in terms of cash flow, a HELOC is the way to go. If you’re looking for the biggest interest savings, a new mortgage is a way to go.

Our mortgage experts can help you determine the best option.

Saving on Interest

If you’re locked into a mortgage at a high fixed rate, you might consider refinancing to save on interest. You do this by signing up for a mortgage at a lower interest rate. If you have enough equity in your property, you could add the mortgage penalty on top to not have to pay anything out of pocket.

The Costs and Fees of Refinancing Your Mortgage

Before refinancing your mortgage, it’s important to be aware that there are costs and fees involved. We’ve already mentioned the mortgage penalty. Another cost is the appraisal.

Usually, lenders will require that you get an appraisal on a property you want to refinance. The appraisal will usually be your responsibility to pay for.

A third cost is the legal costs. You’re looking at about $1,200 in legal costs if you refinance your mortgage through a lawyer. This can be added to the new mortgage, so you don’t have to pay it out of pocket.

The Bottom Line

This article was to give you a glimpse of what a refi is. In our next articles, we’ll be looking at the individual reasons to refi in further detail.