When you’re applying for a mortgage, it’s important to understand some of the concepts and terms. You’ll often hear about fixed and variable rate mortgages. If you read our last week’s article, you may already have a pretty good understanding of those terms. However, there are other important concepts to know, like Mortgage Term and Amortization.

What’s the difference? Let’s take a look at both of them, so you can understand them when shopping for a mortgage.

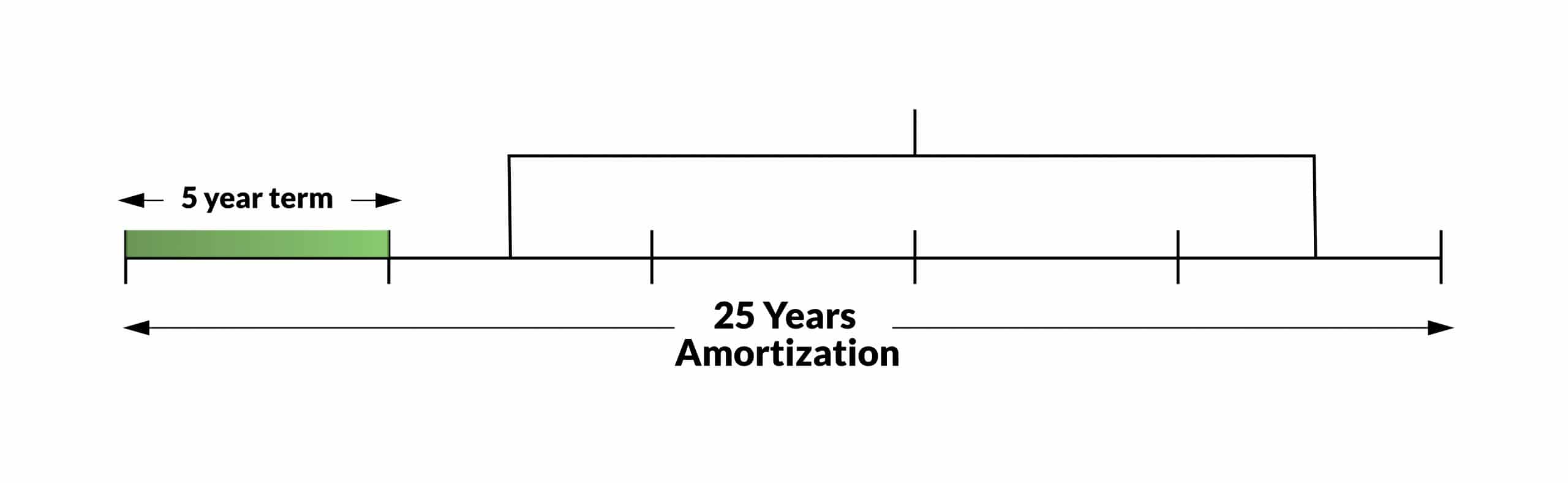

Mortgage Term

The mortgage term is the length of time of the mortgage contract between you and the mortgage lender. For example, if you have a fixed-rate mortgage, your mortgage payment and rate will stay the same until your mortgage term ends. If you have a variable rate mortgage, it works slightly different.

With a variable rate mortgage, your rate fluctuates up and down based on the prime rate. For instance, your variable rate could be P – 0.5%, this means that your rate would be equal to Prime minus the 0.5% (also known as a discount). While your mortgage rate can change, your discount off Prime is part of your mortgage contract with the lender and thus won’t change.

When you sign up for a variable rate mortgage, the rate is quoted as Prime plus/minus a spread.

For example, if your variable rate mortgage is Prime less 0.50% (P-0.5%) and Prime Rate is 2.45%, then your mortgage rate would be 2.45% - 0.5% = 1.95%.

Will your mortgage payments increase when Prime increases?

Not necessarily. There are two types of mortgage payments. ConstantPayment and VariablePayment. With a constant payment mortgage, your payments are constant even if you have a Variable rate. Since mortgage payments are blended (interest and principal) if when Prime increases, only the interest portion of the payments are increased while less will be allocated towards the principal, keeping the payment amount constant.

Normally you’ll have several terms in the life of your mortgage before you pay it off in full. When each term ends, you have to renew your mortgage and you can shop around and switch mortgage lenders if necessary.

Amortization

Your mortgage amortization is how long it takes until you fully pay off your mortgage. The typical mortgage comes with an amortization period of 25 years. That being said, nothing is stopping you from choosing a shorter or longer amortization period.

If you’re putting less than 20% down on a property and getting an insured mortgage, the maximum amortization period is 25 years.

However, if you’re putting down more than 20%, you can go with an amortization period as long as 30 years with most lenders.

The benefit of going with a longer amortization period is that your mortgage payments are lower, helping you from a cash flow standpoint. The downside is that since you’re stretching out the period of time it takes to pay off your mortgage, you’ll incur more interest over the life of your mortgage.

Another choice is to go with a shorter amortization period. Instead of 25 or 30 years, you could go with an amortization period of 22 years or whatever you choose.

By going with a shorter amortization period, you’ll pay less interest over the life of your mortgage. The downside is that your mortgage payments will be higher. You’ll also have to be able to pass the mortgage stress test at the higher payments.

When you make lump sum payments and increase your payment, you’re reducing your amortization period. The main benefit of this is if you run into financial difficulty later on, you could always decrease your mortgage payments to the original amount and stop making lump-sum payments.

We Help You to Find The Best Mortgage Rates

Make a request to speak to a mortgage professional