Do you find compound interest complicated? You’re not alone. In this article we’re going to help demystify the compounding of interest of mortgages.

We’ll look at the posted rate versus effective rate and semi-annual versus monthly compounding.

After reading this article you’ll have a better understanding of the compounding of mortgage interest and be able to better compare mortgage products.

Posted Rate vs. Effective Rate

What would you think if we would tell you that the actual interest rate on your mortgage is more likely higher than the interest rate you were initially quoted? This is due to a couple of factors: your payment frequency and how often your mortgage compounds.

There’s a misconception out there that by paying your mortgage payments more frequently, you’ll save yourself a lot of mortgage interest. While you will save some interest, it’s pretty negligible. What can have a bigger impact on your total cost of borrowing is how often your mortgage compounds.

When the interest on your mortgage compounds, any unpaid mortgage interest is added to the principal amount of your mortgage and a new interest amount is calculated. This results in an interest on interest. The more often your mortgage compounds, the more total interest you’ll pay over the life of your mortgage.

There are two main rates quoted to borrowers: the posted rate (or the advertised rate) and the effective rate (the real rate or APR). The posted rate is the interest rate we most often see advertised, but its shortcoming is that it doesn’t take into consideration compounding.

If you want an interest rate that does, you’re looking for the effective rate, which is seldom advertised. (It’s most often buried in the disclosure documents you’ll receive later.)

Semi-Annual vs. Monthly Compounding

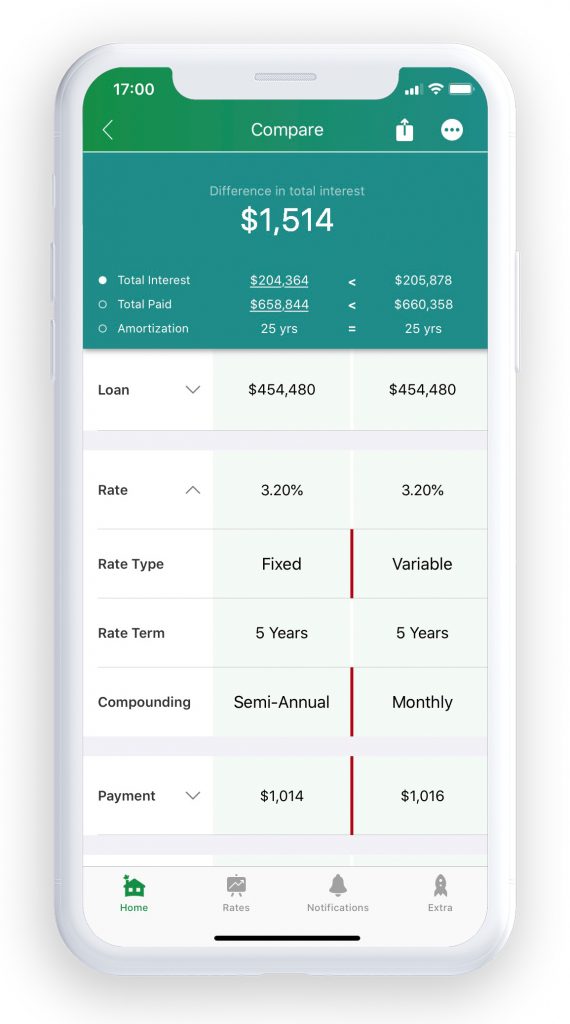

How often your mortgage compounds depends on the type of mortgage you’re taking out. In Canada there are two main mortgage types: fixed and variable rate.

Most Canadians are aware that with a fixed rate mortgage, the mortgage interest almost always compounds on a semi-annual basis (twice a year). But did you know that the compounding on variable rate mortgages is usually different?

A variable rate mortgage typically compounds on a monthly basis. If you have a variable rate mortgage like this, it means that interest is added to the principal amount of your mortgage 12 times a year instead of only twice a year.

Because of this, if we see a 3.2% mortgage rate being advertised for both 5-year variable rate and 5-year fixed rate mortgages, the effective rate on the variable mortgage is always going to be higher than the fixed mortgage because it compounds monthly instead of only semi-annually.

[supsystic-tables id=1]

The Bottom Line

The next time you’re shopping for a mortgage and you see a posted rate that you like, take the time to read the fine print. Find out if it’s the effective rate. (In most cases it won’t be.)

If it’s not, ask the lender to provide you with the effective rate. Also ask about how often the mortgage compounds.

At today’s record low mortgage rates, compounding doesn’t have as much of an affect it did once, but every single penny counts. The higher your mortgage balance, the more of an impact the compounding will have on your mortgage.

Make a request to speak to a mortgage professional