To qualify for a mortgage loan, you will need to pass a “Stress Test.” Passing this test proves you can afford mortgage payments at a higher interest rate than you are being quoted by a lender or a bank.

The Stress Test was introduced by the Office of the Superintendent of Financial Institutions in 2016 and then updated in 2017 and then updated again in 2018. The goal of the stress is to make sure that your income was able to service the debt when rates were increased.

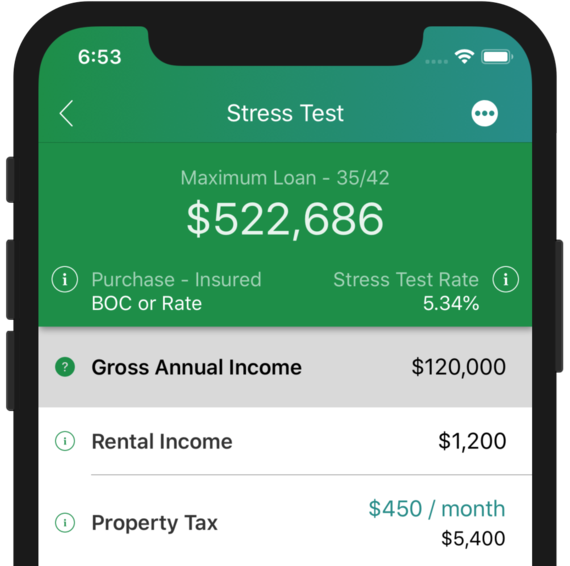

The Canadian Mortgage App is the first-ever app that consolidated the rules into a convenient feature on an app so you can quickly determine the maximum loan you can afford.

Calculate your Maximum Loan

Simply add your annual income, and some details about the property you are purchasing and view the maximum loan you can borrow.

CMA follows all the B-20 guidelines suggested by the Residential Mortgage Underwriting Practices and procedures by the Office of the Superintendent of Financial Institutions of Canada to estimate the loan amount for you.

You can even customize the settings and change the maximum debt service ratios to see how your purchase power changes from one lender to another.

CMA Supports the entire B20 Guideline

Stress test rules don’t apply the same way for all types of mortgage scenarios. For instance, if your house price is over $1 million it works differently than if your house price is less $1 million and your down payment is less than 20% (ie insured mortgage).

Receiving rental income affects how much loan you can qualify. In fact, there are several ways rental income can be used. (A) Certain % can be added to your gross annual income or (B) Certain % can be added to reduce your expenses and then the remainder added to your income.

CMA is the first app that has developed the ability for you to see how your overall borrowing power changes with rental income.