How much do you "actually" save when you pay your Mortgage sooner?

With mortgage rates increasing, you may think of ridding yourself of your mortgage debt sooner rather than later. You’re not alone. Let’s look at three simple ways to pay down your mortgage sooner.

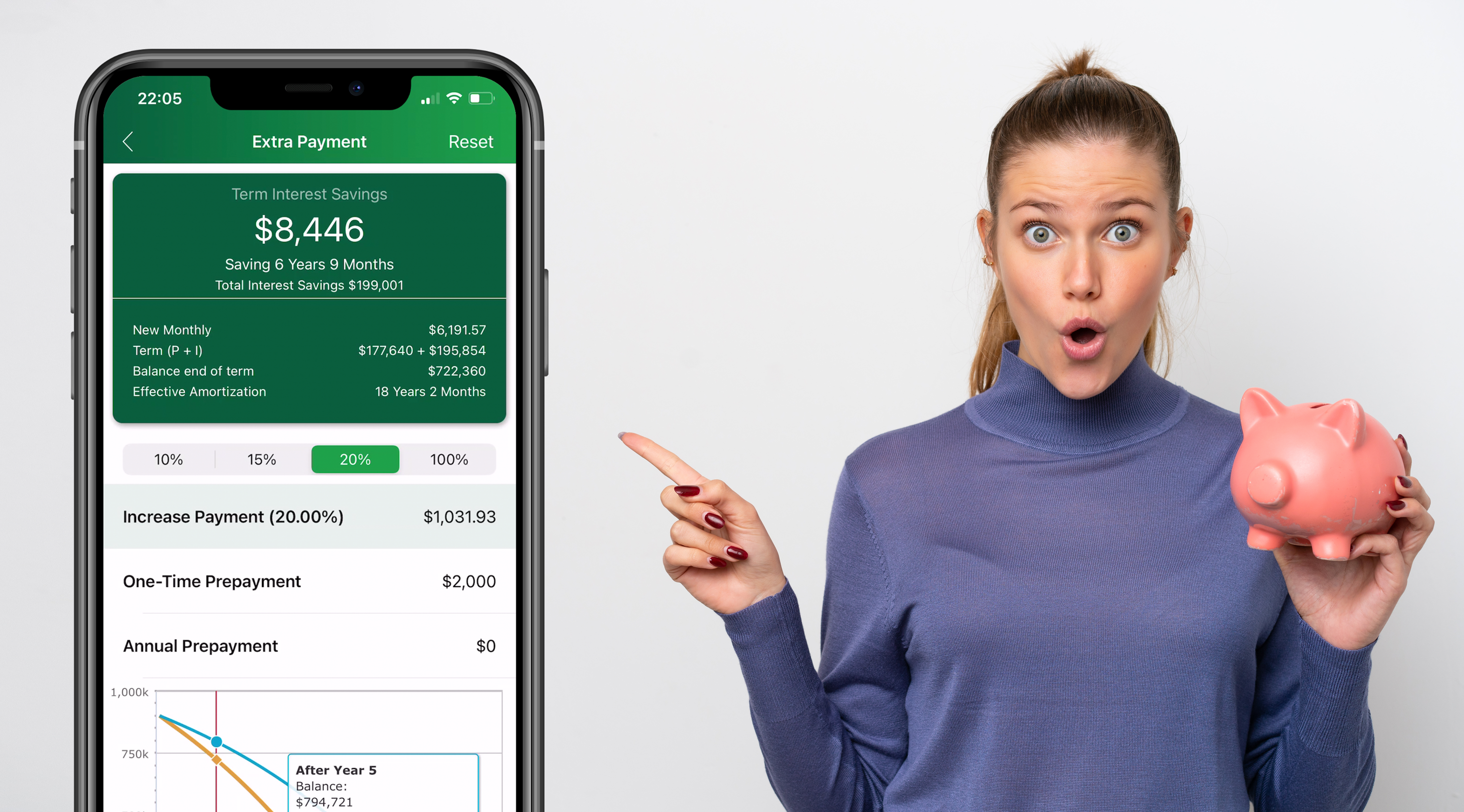

Increase Payment

Do you have extra money at the end of the month and are unsure what to do with it? If you leave the money sitting in your savings account, you’re most likely losing money since savings account rates tend to be much lower than the rate of inflation. If you have a mortgage rate in the 4% or 5% range, you can get a much better return by putting the money against your mortgage.

Increasing your payment makes sense if you have extra money at the end of each month and want to pay off your mortgage faster without thinking about it. When you increase your payment, your mortgage payment is automatically higher, without you needing to do anything or think about it.

Most lenders are flexible. You can increase your payment by $50, $100 or whatever you can afford. Unlike a regular mortgage payment split between principal and interest, that extra $50 or $100 goes entirely towards the principal, helping you pay down your mortgage much faster.

One-Time Payment

The second option is a one-time payment. Let’s say you receive an unexpected one-time chunk of change. Maybe it’s a spot bonus at work. Perhaps it’s a one-time inheritance. Whatever the reason, you can choose to put some or all that money toward your mortgage.

The beauty of a one-time payment is that, like increasing your payment, the one-time fee entirely goes toward your principal. If your mortgage balance is $500,000 and you make a $2,000 lump sum payment, your balance will be $498,000. It’s as simple as that.

You’ll also pay less interest on your mortgage over its lifetime, as the interest is calculated on a lesser balance. It’s a win-win situation.

Annual Prepayment

The third way to pay down your mortgage sooner is to make annual prepayments. Instead of receiving a one-time amount, let’s say you expect to receive the same amount each year. Examples of this include a tax refund or workplace bonus.

Like a one-time payment, when you make annual prepayments, the amounts go entirely towards reducing the balance on your mortgage. And doing it over time adds up in terms of principal and interest savings.

How the Canadian Mortgage App Can Help

With the Canadian Mortgage App, you can use all three methods to see how much interest you’d save.